When you’re involved in a collision with someone who lacks proper insurance coverage, the situation transforms from challenging to potentially devastating, depending on which state you call home. Florida and Texas handle uninsured motorist accidents very differently, and understanding these distinctions can mean the difference between recovering full compensation and being left to cover thousands in expenses yourself.

Car accidents are unpredictable enough without the added complication of an uninsured driver. At Amanda Demanda Injury Lawyers, we handle complex injury claims across both Florida and Texas, and we understand how these state-specific insurance laws impact accident victims. Our experienced team works to protect your rights and pursue maximum compensation, regardless of the at-fault driver’s insurance status.

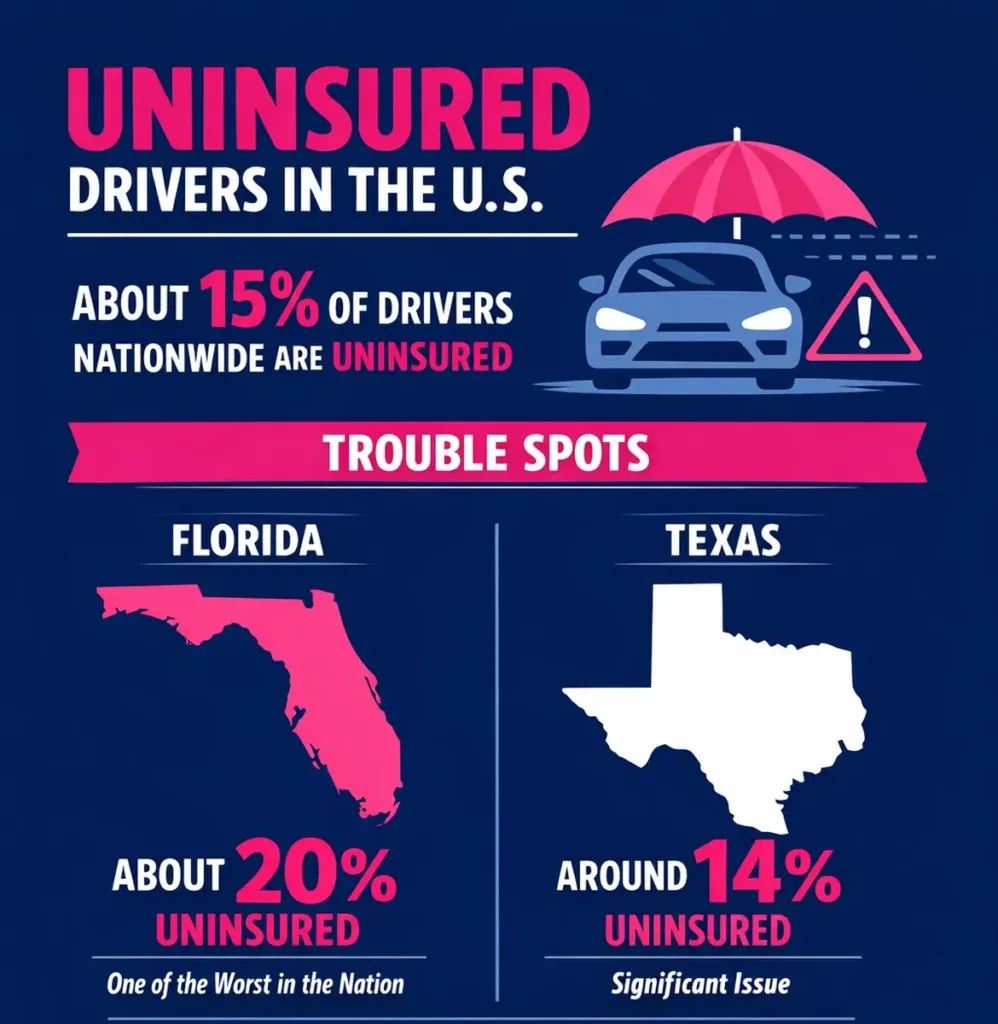

The Uninsured Motorist Problem in Both States

Uninsured drivers represent a significant risk on roads nationwide. According to the Insurance Information Institute, about 15% of drivers nationwide were uninsured in 2023. However, the problem is particularly acute in Florida and Texas. Florida struggles with an uninsured motorist rate of around 20%, making it one of the worst states for this issue. Texas reports a rate around 14%, which aligns with the national average but still translates to hundreds of thousands of drivers without adequate coverage.

Florida’s No-Fault System Creates Unique Challenges

Florida operates under a no-fault insurance system, which creates a distinctive framework for handling car accident claims. When you’re injured in Florida, you first turn to your own Personal Injury Protection coverage, commonly known as PIP insurance. This coverage pays up to $10,000 and covers up to 80% of medical expenses and 60% of lost wages, regardless of who caused the accident.

Florida’s no-fault system includes an important exception. You can step outside the no-fault limitations and file a lawsuit against the at-fault driver if your injuries meet the state’s serious injury threshold. This includes permanent injuries, significant scarring, or cases requiring emergency medical treatment within 14 days of the accident. When the at-fault driver has no insurance, this creates a significant problem because there’s no insurance company to pursue for damages beyond your PIP coverage.

While Florida mandates PIP coverage, it does not require drivers to carry uninsured motorist coverage. This optional coverage becomes your financial safety net when an uninsured driver injures you. If you have UM coverage, your own insurance company compensates you for damages exceeding your PIP limits, including pain and suffering, which PIP doesn’t cover. Without this coverage, your only recourse may be to collect directly from the at-fault driver, which is often fruitless because many uninsured drivers lack significant assets.

Texas’s At-Fault System Offers Different Protections

Texas takes a fundamentally different approach with its traditional at-fault insurance system. When you’re injured in a Texas car accident, you have the right to pursue compensation directly from the at-fault driver’s insurance company. This system provides more straightforward access to full damages, including medical expenses, lost wages, property damage, and pain and suffering.

Texas requires drivers to carry liability insurance with minimum limits of $30,000 per person and $60,000 per accident for bodily injury. However, these requirements only matter if the at-fault driver actually maintains coverage. When they don’t, you face the difficult reality of having a valid claim but no insurance company from which to collect.

Texas law requires insurance companies to offer uninsured motorist coverage, though drivers can reject it in writing. This coverage mirrors your liability limits and activates when an uninsured driver injures you. Your UM coverage essentially steps into the shoes of the at-fault driver’s nonexistent insurance, allowing you to recover compensation without pursuing the lengthy process of collecting from an individual.

What to Do After Being Hit by an Uninsured Driver

Getting medical attention should be your first priority, even if your injuries seem minor at first. Many serious injuries don’t manifest symptoms immediately, and prompt treatment creates important documentation for your claim. While at the scene, try to gather as much information as possible, including photographs, witness contact details, and the other driver’s information.

Filing a police report helps establish an official record of what happened. You’ll also want to notify your insurance company about the collision relatively quickly, as delays can sometimes complicate your claim. Take time to review your insurance policy and determine whether you have uninsured motorist coverage, which becomes crucial in these situations.

Contacting an experienced personal injury attorney can make a significant difference in securing fair compensation. Insurance companies often minimize uninsured motorist claims, and having legal representation helps protect your interests throughout the process.

Trust Amanda Demanda Injury Lawyers With Your Uninsured Motorist Claim

Dealing with an uninsured motorist accident adds to the frustration of an already difficult situation. At Amanda Demanda Injury Lawyers, we handle these cases across Florida and Texas with locations in Miami, Tampa, and Houston. We understand the nuances of both state systems and work aggressively to maximize your recovery, whether that means negotiating with your UM carrier or pursuing other available remedies.

Attorney Amanda Demanda and our experienced legal team know how to build compelling claims that demonstrate the full extent of your damages. Contact us today to schedule a free consultation and discuss your uninsured motorist claim.

Back to Blog